As the 2025 tax filing season is upon us, many people feel stressed about getting income tax

returns completed correctly and on time. This article will provide an overview of how federal

income taxes work in the United States. Hopefully, this knowledge will help give everyone a

better understanding of what goes into a tax return, even if you are not preparing your own

return personally.

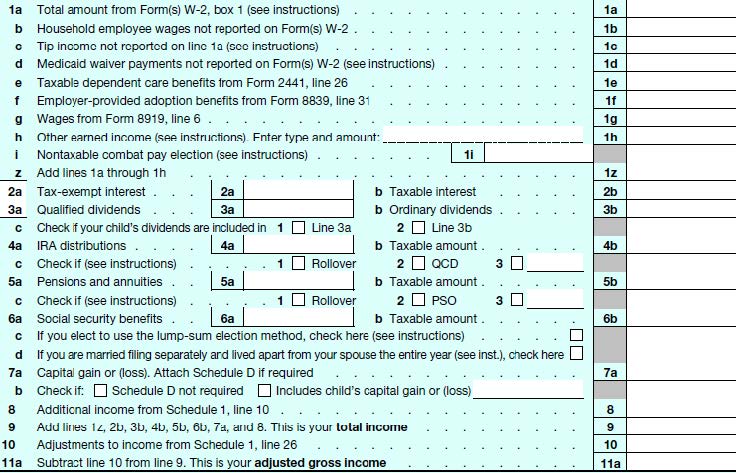

The main form used to report income to the Internal Revenue Service (IRS) is Form 1040 –

U.S. Individual Income Tax Return. There is a simplified Form 1040-SR for filers over age 65

but this article will refer to the standard 1040. U.S. citizens are taxed on all income earned for

the year, whether it is earned domestically or abroad. There are a multitude of sources that

taxpayers can earn from but the most common one is employer-paid income documented by

a W-2. The majority of workers in the country are paid a salary by a company, which is

documented by the employer each year on Form W-2, showing total payments and

additional information on state, federal, Social Security, and Medicare taxes withheld as well

as any other deductions like 401(k) contributions.

Retirement income such as payments from pensions or Social Security, as well as distributions

from pre-tax retirement accounts such as IRAs, are logged in sections 4-6 of the form.

Notably, only a maximum of 85% of Social Security benefits are subject to income tax, so the

gross benefit amount in box 6a should always be greater than the taxable amount reported in

box 6b. You can also note in these sections if a distribution from a retirement plan (say, a

rollover from a 401(k) to an IRA or a qualified charitable distribution) should not be taxed as

income.

Other, less common, types of earned income are also reported somewhere in this section of

the 1040. If necessary, a Schedule 1 is included to document other income sources like

rental real estate and business/partnership income that is distributed via a document known

as a K-1 that divvies up the total business income across its owners/partners. All of the

additional income that flows through Schedule 1 ends up in box 8 of the 1040.

Investment income earned in a non-retirement account (bank account, brokerage account)

also needs to be reported. Whenever you divest from interest in a capital property (real

estate, stocks, bonds, etc.), that generates a gain or loss that can affect that year’s taxable

income. Interest and dividend income go in sections 2-3 while capital gains from the sale of

aforementioned property are shown in section 7.

To get from total income to adjusted gross income (which the tax amount is based on), there

are some adjustments that can be made on Schedule 1. The most common are Health

Savings Accounts contributions, deductible IRA contributions, student loan interest

deductions, and deductible alimony paid. Once all this income and any relevant adjustments

are accounted for, you have completed the first page of your return!

Once you have total income in hand, the next page of the 1040 turns to deductions. The Tax

and Credits section first reduces your AGI by any appropriate deductions and then calculates

the total tax owed on that final income number shown in box 15. Every taxpayer is entitled to

a standard deduction ($15,750 for single filers and $31,500 for married taxpayers in 2025).

This is a freebie deduction that reduces your AGI and contributes to a lower tax bill. There

are additional deductions available if over age 65 and/or blind. If allowable itemized

deductions—from charitable giving, mortgage interest, state/local taxes, medical expenses

above 7.5% of AGI—are greater than the standard deduction, you can reduce your income by

that higher itemized deduction figure. For 2025 tax filing, the cap on deductible state and

local taxes has increased from $10,000 to $40,000 as long as your income is not too high so

this may lead to more people itemizing this year than before.

The calculation of federal taxes owed is usually best left to software or a professional

preparer, as not all income is assessed at the same rate. For example, earned income from a

W-2 is subject to the normal tax brackets but capital gains from realizing a profit on an

investment has different rates based on what your total income was for the year. A common

misconception is that once your income moves into a new tax bracket, then all your income is

charged that higher rate. In reality, the United States uses a progressive tax system, where

only the income in each bracket pays that rate. This means, if you go $10 over the 24%

bracket income level, only that $10 is charged the next bracket rate of 32% and all previous

income will pay 24% or less.

The Payments and Refundable Credits section settles your tax amount owed from the

previous section with all payments already made for the year. Frequently, taxpayers will

prepay most of their tax bill, either through tax withholding from paychecks or estimated tax

payments made over the course of the year. Sections 25-26 of the 1040 ensure you receive

credit for all of these prepayments. Any applicable additional credits are then added on to

the prepayments and the difference between these total payments and total tax owed

constitutes the refund amount or balance due. If you find yourself either with large balances

owed or sizeable refunds every year, it may make sense to adjust prepayments (withholding

from paychecks, estimated payments, or both) in order to avoid underpayment penalties for

not making enough prepayments as well as giving the government an interest-free loan,

which is essentially what is happening when too much withholding is taken throughout the

year and a large refund is paid back the following spring.

While the tax return documents and all the paperwork required can be intimidating, it really

just breaks down to adding up your income, calculating any allowable deductions or credits,

and then reconciling the resulting tax amount calculation with your payments made

throughout the year to determine how much you owe or are owed. We would be happy to

take a deeper dive into your specific situation if you have more intricate questions about your

taxes.

Reach out today. This could be the start of a great relationship.

Contact Us